Evolution of sales in the textile sector: resilience and opportunities since 2020

For decades, Europe was synonymous with creativity, quality, and leadership in global fashion. From its workshops, runways, and design studios emerged trends, materials, and standards that set the pace of global consumption. However, that balance has been disrupted by the emergence of ultra-fast fashion, a model driven by giants such as Shein, Temu, Cider, Boohoo, Missguided, Pretty Little Thing, Zaful, Fashion Nova, or Amazon Haul, which has redefined the rules of the market, provoking regulatory pressure, unfair competition, and new challenges in sustainability and compliance.

Despite this disruptive context, the European textile sector has shown remarkable resilience since 2020. According to EURATEX reports, turnover in the European Union fell by 19% in 2020 (to 147 billion euros) due to the impact of the pandemic, but rebounded by 7% in 2021 and experienced strong growth of 10% in 2022, exceeding 170 billion euros. In 2023–2024, sales stabilized with increases of 0–2% (around 175 billion), and for 2025, a growth of 2–4% was projected, driven by exports and sustainable segments with great expectations at the end of the year.

At a global level, the International Textile Manufacturers Federation (ITMF) reports a 15% recovery between 2021 and 2022, while in Spain, data from Acotex show a 5–7% rebound in 2022–2023 and stability in 2024, with positive forecasts by the end of the year. Meanwhile, the McKinsey report State of Fashion 2025 confirms this trend: although the market is stabilizing, Europe continues to lead in creativity, design, and premium fashion, with broad opportunities in sustainable innovation that position it as a global powerhouse.

However, the impact of ultra-fast fashion has left a mark: in just three years, the average gross margin of the European textile sector has dropped from 48% to 34%, revealing the pressure of a model based on speed and low cost.

From SODS ESTUDIO, we present an analysis based on sectorial data for 2025 with special emphasis on regulatory compliance as a differential factor.

From speed to disruption

The ultra-fast fashion model is based on the constant updating of its catalog (thousands of new products every week), digitally adjusted prices, an almost immediate response to trends, and logistics that take advantage of European regulatory loopholes. The average gross margin has fallen from 48% to 34% in three years, and traditional brands are losing ground to companies capable of renewing garments and sales cycles in a matter of days. Among the main players are:

-

- Shein: the absolute leader, with more than 12 million daily orders worldwide and projected revenue of 58 billion dollars in 2025. Its test-and-repeat model allows it to introduce up to 10,000 new products each day, adjusting production in real time to demand detected by predictive algorithms.

- Temu (PDD Holdings): With 200,000 daily shipments to Europe, it will reach 35 billion dollars in revenue this year, thanks to its group-buying model and ultra-competitive prices.

- Boohoo, ASOS, or Pretty Little Thing: major exponents in Europe that replicate trend analysis and test-and-repeat algorithms, differentiated from traditional fast fashion by their responsiveness and scale.

- Amazon Haul: the U.S. giant competes in Europe with an ultra-low-cost offering driven by predictive analysis and viral hauls, with planned expansion in the EU and the United Kingdom during 2025, putting pressure on local brands.

- Taobao, AliExpress, and Tmall Global (Alibaba Group): together they account for more than 40 billion dollars in fashion sales, driven by live commerce strategies and direct-to-consumer distribution.

- Pinduoduo, Zaful, and Romwe: strengthen the youth and low-cost offering, with annual growth rates above 15%.

- Xiaohongshu (Little Red Book): merges social commerce and luxury fast fashion, generating around 500 million dollars in cross-border sales.

The result is a structural market distortion, where European companies, bound by strict EU compliance frameworks, compete at a disadvantage against global players with unbeatable costs and minimal traceability.

Consumption: between convenience and contradiction

The rise of ultra-fast fashion is not a spontaneous phenomenon: it reflects a transformation in global consumer habits. According to the report The State of Fashion 2025 prepared by McKinsey & Company and The Business of Fashion, the loss of purchasing power and the increase in price sensitivity – what the authors define as value-conscious spending – are the main catalysts for the growth of this model.

Inflationary pressure, rising energy costs, and wage stagnation have changed the priorities of millions of European consumers, who now seek “more for less”. This shift has caused price to surpass previously decisive factors such as quality, traceability, or product origin.

According to McKinsey, more than 60% of consumers in markets such as Western Europe, the United States, and the United Kingdom state that they try to spend less on fashion, and more than 45% claim they turn to Asian digital platforms to find cheaper alternatives.

It is estimated that the ultra-fast fashion segment is the only one in the textile sector that will grow above 15% annually in 2025, in contrast to the flat or negative growth of traditional brands. This trend consolidates the transition from aspirational consumption to purely functional consumption, where the perception of value is associated with cost rather than durability.

But behind this phenomenon lies a paradox: this same report indicates that the same consumer who demands sustainability and social responsibility is rewarding, through purchasing decisions, the most opaque, intensive, and difficult-to-monitor models.

The evolving consumer: academic insights for 2025

In 2025, fashion purchasing behavior is transforming toward hyper-personalized and proactive decisions, driven by AI engineering. Recent studies highlight how predictive algorithms compress the customer journey, shifting it from impulsive to functional and sustainable.

For example, research from the University of Virginia (Darden School of Business) indicates that around 60–70% of consumers trust AI recommendations for fashion purchases, accelerating decisions and prioritizing ecological options.

A study by Atma Jaya Catholic University (Indonesia) and Chung Yuan Christian University (Taiwan), published in Sustainability (2025), reveals that AI personalization increases green purchase intent by approximately 10-15% among young people.

Doctors in social sciences from the University of Algarve (Portugal) analyze how analytical technologies (big data, e-WOM) amplify social influences, raising confidence in online shopping by 20–40% when moderated by habits and transparency.

These insights predict for 2025 a shift toward community-based and green shopping, where AI acts as a “trusted advisor”, but they warn of risks if traceability is lacking.

Fast fashion or ultra-fast fashion? Differences and challenges

Unlike the nature of more traditional fast fashion brands, for example:

Ultra-fast fashion has taken the speed of consumption to a new extreme, renewing its catalog daily instead of by seasons or weeks, through algorithms capable of identifying and replicating viral trends in real time. Brands in the sector launch micro-productions under a test-and-repeat model that allows them to adjust prices and volumes almost by the second, reducing inventories but multiplying turnover.

This model has not only accelerated consumption, but has also redefined the very concept of production: where once there were seasonal collections, today there are thousands of weekly launches. The logic of “see, want, buy and discard” has become the driving force of a system in which immediacy outweighs quality, cost outweighs traceability, and clicks outweigh value.

In response, brands operating within the European framework and committed to social responsibility toward the end consumer are adopting more agile processes and a firm commitment to sustainability. However, their pace and profit margins cannot compete with the speed or costs of the ultra-fast model.

Regulatory impact: the new European horizon

Institutional reaction is already underway. The European Union has taken on the challenge of curbing the impact of ultra-fast fashion with a new regulatory agenda that combines sustainability, taxation, and traceability. Within this framework, the reform of the European Customs Code will end the 150-euro exemption, imposing effective controls and VAT payment for all non-EU shipments.

France, for its part, has gone a step further with the creation of a progressive environmental tax for low-cost garments, penalizing products with greater ecological impact and limiting advertising that encourages impulsive consumption.

These measures are joined by new European directives on sustainability and transparency, which shape a new regulatory horizon for the textile sector:

-

-

- The Corporate Sustainability Reporting Directive (CSRD) will require thousands of companies will oblige thousands of companies to report their environmental and social impacts with verifiable criteria.

- EPR fees on textile waste will establish circularity and extended producer responsibility obligations.

- The Eco-Design Directive (ESPR) will will promote more durable, repairable and recyclable products. With this set of reforms, among others, Europe seeks to level the market and prioritize traceability, circularity and corporate responsibility.

-

But these rules not only demand adaptation: they also open the door to a new kind of corporate leadership—one that understands compliance not as a legal requirement but as a corporate culture that generates trust, competitiveness, and long-term value.

Sustainability and compliance: from obligation to competitive advantage

Ultra-fast fashion has a high invisible cost: more emissions, more waste and precarious working conditions in Asian production centers. In the European Union, each person generates 16 kg of textile waste per year, but only a quarter is recycled or reused. Behind every low-priced garment there is an environmental and social footprint that is rarely seen, but which reflects the true impact of a model based on immediacy and discarding.

In this context, the compliance and digital traceability are no longer an option, but a shield and a strategic asset. Companies that integrate audits, ESG reporting and real circularity not only comply with regulations: they differentiate themselves, gain access to incentives and strengthen a solid and trustworthy reputation .

Designing the future with responsibility

European fashion is undergoing a moment of profound change. Speed and cost can no longer prevail over control and ethics, and the European Union is setting the course towards a model where only companies capable of combining agility, innovation and regulatory compliance will be truly competitive in the face of the ultra-fast fashion phenomenon.

Convert the compliance into corporate culture is no longer an option, but the key to sustainability and trust. Organizations that integrate responsibility into their strategy not only comply with the law: they build value, credibility and long-term resilience.

An additional challenge facing the textile sector is the large and growing second-hand market, especially online with portals such as Vinted (a leader in affordable casual fashion) and Vestiaire Collective (specializing in pre-owned luxury). According to recent reports by BCG and Vestiaire Collective (2025), this market is growing 10% annually, three times faster than first-hand fashion, reaching $208-220 billion in 2025 and projecting $360 billion by 2030. Driven by environmental and economic awareness, it represents 10% of the global market by 2025, eroding new sales, but fostering circularity. For traditional brands, this implies hybrid strategies: integrating resale to capture sustainable audiences and aligning with EPR regulations.

This growth reflects a greater social awareness in purchasing: consumers opt for second-hand not only to save money (up to 70% less), but also to reduce their ecological footprint (less waste, reuse) and promote ethics (support for local economies, anti-overconsumption).

Studies show that 67% of millennial shoppers prioritize sustainability, driving platforms that verify authenticity and quality. In Europe, this aligns with ESPR and EPR regulations, turning resale into an opportunity for brands that offer durable and traceable products, driving social value and brand engagement.

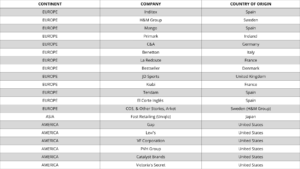

Most purchased pre-owned Items – Ranking 2024-2025 in order from highest to lowest:

The challenge: balancing physical store (sensory experience) with AI (instant personalization), preventing the latter from eroding the customer relationship.

With proven resilience since 2020, the European textile sector is not only regaining ground, but positioning itself for qualitative growth, driven by innovation and responsibility.

What to do? From SODS ESTUDIO, we help anticipate regulations, consolidate supply chains, transform compliance into an operational advantage and bring novelty to outerwear collections, accompanying companies in their transition to a model aligned with European standards.

Everything in our industry revolves around the end product and, above all, the ability to listen and respond to what our customers really want.